Google’s dominance over the smartphone landscape appears to be topping out, but the company is gaining more control over the devices that run its software.

The Android mobile operating system ran 84% of smartphones shipped globally in the third quarter, according to research firm Strategy Analytics, down slightly from 85% in the second quarter.

“Android’s global smartphone market share is peaking,” said Strategy Analytics analyst Neil Mawston. “Unless there is an unlikely collapse in rival Apple iPhone volumes in the future, Android is probably never going to go much above the 85% global market share ceiling.”

Market share for Apple’s iOS mobile operating system was 12% in the third quarter. Microsoft ‘s Windows Phone captured 3% share and BlackBerry devices 1%.

A Google employee displays a nexus 6 smartphone during a media preview in New York on October 29, 2014.

Even if Android’s market share doesn’t go any higher, there is still good news for Google.

For starters, the market overall is still growing. Strategy Analytics forecasts 12% growth in smartphone shipments in 2015.

Second, Google appears to be turning the tide on the growth of so-called Android forks – versions of the mobile operating software that are developed independently and don’t come with Google’s lucrative mobile apps.

As a percentage of total Android shipments, forks made up 37% in the third quarter, down slightly from 39% in the second quarter.

Google makes no money on Android itself, since it gives away the operating system for free to device makers. It profits from revenue generated by advertisements that appear in apps like Google Search, Google Maps and YouTube, as well as a cut of sales of apps, files, subscriptions, and the like sold through the Google Play Store.

Mr. Mawston of Strategy Analytics chalks up the decline in Android forks to a “maturing” China smartphone market, where most forked Android devices are sold. In addition, Google is asserting control over its operating software through its newly launched Android One program. That program is designed to provide cheap, reliable smartphones to consumers in emerging markets such as India. Those phones come with Google’s various services installed.

Meantime, Samsung’s dominance over other Android handset makers is waning, reducing the threat that the Korean hardware maker could wrest more control from Google. In the third quarter of this year, 25% of smartphones shipped were Samsung devices. That figure cratered from the year prior, when it stood at 35%.

Samsung ships mostly Android devices and long has been dominant among Android vendors thanks in part to big commissions it pays to smartphone distributors, particularly in emerging markets. That gives them an incentive to push its devices over rivals.

Yet Samsung is losing out to upstarts like China’s Xiaomi, which are undercutting the Korean giant on price. Samsung sells its smartphones at a premium and captures bigger profit margins on each device sold, while Xiaomi prices its devices closer to the cost of making them and profits instead on the sale of accessories and software add-ons.

In the previous two years, as Samsung’s market share peaked, it tried to assert more independence from Google by distributing more of its own services on its Android devices while simultaneously downplaying the fact that Google’s software powered them. That sparked concerns inside Google that it could lose some control over the operating system, according to people familiar with the company’s internal deliberations.

Earlier this year, Samsung and Google reached a detente of sorts, when they agreed to a broad patent cross-licensing deal.

The biggest challenge to Google’s mobile dominance could come from regulators. European Union antitrust authorities are poised to unleash a formal investigation into Android in the wake of concerns that Google shuts out rivals in promoting services such as Google Maps.

The Wall Street Journal first reported the news of Google’s secret agreements with handset makers requiring them to feature those services prominently if they want access to the services in the first place.

President Goodluck Jonathan, Dr. (Mrs.) Omobola Johnson, Galaxy Backbone Limited and other prominent Nigerians who have contributed in positioning the ICT industry as the greatest driver of the Nigerian economy within the century, were rewarded with garlands of honour, at the first ever ICT Centenary Conference and Awards, which held at the Shehu Musa Yar’Adua Centre, Abuja recently.

At the event which had in attendance top industry administrators, operators, regulators, and enthusiasts, the President was honoured with a trophy as the “Grand Commander of ICT Promoter” at the event organised by the ICT Media Initiative. The award was received on behalf of the President by the Minister of Communication Technology, Dr. (Mrs.) Omobola Johnson.

Mrs. Omobola Johnson Hon. Minister of Communications TechnologyPresident Goodluck Jonathan

Other awardees included Nigeria’s Minister of Communication Technology, Dr.(Mrs) Omobola Johnson who took away the trophy as the “Premier ICT Officer of the Federation”, while Galaxy Backbone Limited went home with the award for promoting Whole-of-Government approach in Information Age.

The award is in recognition of the consolidation and expansion of government-wide ICT infrastructure by Galaxy under its “1-GOV.net” initiative. 1-Gov.net is a common ICT platform built and operated by Galaxy on behalf of all the Ministries, Departments and Agencies (MDAs) of the Federal Government for the efficient and effective delivery of public sector services.

Receiving the award, Yusuf Kazaure, Galaxy Backbone, Managing Director/Chief Executive Officer, said that, “Galaxy Backbone’s 1-GOV.net initiative came up for recognition because it represents a creative and exemplary solution that is transforming the information technology landscape in the Federal Government and its MDAs into a single, co-ordinated platform for e-government programmes in a space of 8 years.”

1-GOV.net has been recognised because of the role it now plays in enabling other electronic government services for internal government operations such as the automation of the memo handling process for Federal Executive Council meetings; government personnel payroll management (IPPIS) thus resulting in the gradual elimination of ghost workers in the federal civil service; and an IP telephony system which allows for communication within and across government MDAs.

Yusuf Kazaure, MD/CE, Galaxy Backbone Ltd (right) receiving the award at the event in Abuja recently.

1-GOV.net also supports the delivery of public services such as the provision of bridging assistance for the transportation of petroleum products to maintain uniform prices across the country with over 1,000 trucks are processed daily in real time by Petroleum Equalisation Fund; the real time implementation of new biometric drivers licensing scheme nationwide targeting over 20 million drivers by 30th September 2013; and the processing of over 5 million international passengers in 2012 by the Nigerian Immigrations Service.

Galaxy won a similar award from the United Nations Public Service Awards in 2013.

The charter which authorised the existence of Export – Import Bank of the United States (U.S. Ex-Im) was due for renewal at the end of this past September. Its re-authorisation required congressional approval. But the renewal of the charter seemed to have fallen due at the wrong time.

Bipartisan consensus on virtually anything has been difficult to come by for some time now, for reasons that could very easily be linked to the mid-term election in November, 2014. This had made the U.S. Ex-Im to teeter on the brink of dissolution until its charter was extended for nine months pending long-term re-authorisation.

I had expected the renewal of the charter of the Bank to be a seamless exercise. But it wasn’t. Instead, the debate became rancorous and polarised along party lines in the most awkward way.

For instance, President Barack Obama lent voice support to the renewal of the charter. He said every country has an institutional framework like the Ex-Im Bank to support its exports. He also noted that, if the U.S. Ex-Im became defunct, U.S. companies would struggle to compete abroad.

Roberts Orya

This position is a marked departure from when in 2008, as a Democrat senator, Mr. Obama criticised the Ex-Im Bank as a government programme that doesn’t work and “little more than a fund for corporate welfare.”

In another twist of irony, the Republican-dominated House of Representatives has stood in the way of the renewal of the U.S. Ex-Im charter. Whereas it is the Tea Party, mainly conservative Republicans, that traditionally supports business — the very businesses that U.S. Ex-Im is set up to provide funding support to. This tends to demonstrate the fluidity of policy positions that are established by partisan considerations.

Nevertheless, the debate has actually helped to shed more light on the activities of the Bank. Otherwise uninformed U.S. business owners, who want to sell in overseas markets, now know about the specialised bank, which some commentators had described to be ‘little-known outside Washington DC.’

A similar case of institutional obscurity was made, with validity, against Nigerian Export-Import Bank (NEXIM Bank) before I came into office and until we rolled out what remains a robust communication strategy.

Inadequate corporate communication might have led to the accusation that the U.S. Ex-Im was little transparent and accountable. This provides an important learning experience that highly specialised institutions of the state nevertheless need to share information about their activities with the general public.

The U.S. Ex-Im Bank is a Development Finance Institution (DFI) which was chartered to act as the Export Credit Agency (ECA) of the United States. The objective of the Bank is to help U.S. businesses access foreign markets. There are a few tools that have been developed to achieve this objective. They include provision of guarantee, export insurance and buyer credit.

Together, they help make U.S. products to be competitive abroad, since exports of other countries are similarly incentivised, if not subsidised, by their governments. It is this same objective that informs the creation of the ECOWAS Trade Support Facility by NEXIM Bank to assist Nigerian exporters gain more access to the West African market where we compete with exports from China and the European Union.

ECAs help to mitigate the risk of entry into a foreign market. They also help to provide funding to build capacity for export. Thereby, local businesses are able to achieve higher profit and employ more local people. The virtuous cycle that is created by an ECA also entails helping the country to move towards a positive current account position, by reducing trade deficit. By helping to create export markets, an ECA invariably helps in boosting domestic economic growth.

The US Ex-Im has a rich history of performance. The Bank is more than 80 years old. It has since its founding, till now, funded $567 billion of U.S. exports. The Bank has raised its intervention in the past few years, partly because Africa has come under the radar of some U.S. companies. Its intervention in U.S. export amounted to $37 billion in 2013 alone.

The aggregate funding has supported over 1.2 million U.S. jobs over the years. More than 80% of its funding has benefitted small and medium scale enterprises (SMEs). The US Ex-Im also funds big U.S. businesses including General Electric, Caterpillar and Boeing. Funding by the Bank has helped U.S. businesses to innovate and compete in new technology, including renewable energy. What’s more, the bank has been profitable, placing no burden on tax payers in covering its cost of operation.

Considering its good purpose, positive performance, and setting aside politics, one may ask: “why should U.S. lawmakers be reluctant to keep the Ex-Im Bank going?” Some of the answers reveal very little understanding of the unique role an export credit agency plays.

Some people have argued that the U.S. Ex-Im is in competition with the commercial banks. Not really. ECAs usually fund businesses or operations which are considered to be too risky by commercial banks. The businesses might be at an early-stage of growth and exploration of export markets. Without much institutional track-record and operational experience in a foreign market, most businesses cannot expand through conventional bank financing.

They would be dogged by high risk evaluation that will either deny them funding or the price of credit would be too high for their affordability.

In Nigeria, an additional obstacle which conventional finance would pose to the businesses is the predilection of commercial banks for short-term lending. But, a specially mandated DFI like the U.S. Ex-Im or NEXIM Bank would take on these risks and back the businesses on the strength of its balance sheet and sovereign mandate (not necessarily involving issuance of a sovereign guarantee).

Funding by ECAs can prepare a business and help it through the difficult early stages until it is capable of attracting or affording commercial loans. This process can work the other way round at the later stages of the corporate development of a business. A growing business, which had accessed commercial lending from the banks, may nevertheless need a specialised bank to help it access a foreign market. Therefore, the role of an export credit agency is very supportive of both commercial banks as well as local businesses.

Some detractors have talked about excessive risk-taking by ECAs. This claim is based on generalised risk evaluation. Such assessments do not always take into account that ECAs have special risk management tools that are suited to the kind of risk they bear.

For instance, NEXIM Bank makes the point of understanding specific risks of its clients. We follow our clients to the market to understand the peculiar variables that constitute risks to them. We then develop specific products to help address the risks.

Regarding the U.S. Ex-Im, its track record is strong enough to denounce any accusation of excessive risk-taking. Since its founding, the Bank has witnessed episodes of serious financial crises in the domestic, emerging and global markets. Yet, the U.S. Ex-Im has been unscathed in any of them. Its recent non-performing loan is 0.2% of total portfolio.

The accusation of cronyism also derives from a misunderstanding of the role of an ECA. For instance, NEXIM Bank is designated as the Official Trade Policy Bank of the Federal Republic of Nigeria. This means the operations of the bank must necessarily be in alignment with the trade objectives of the government. In this regard, NEXIM Bank has been pushing the programme of economic diversification in the non-oil sectors as enunciated under the Transformation Agenda of President Goodluck Jonathan.

The programme entails the broadening of the export base in order to generate more foreign exchange for the country and create more local jobs. Local industries which are capable of scaling up to help deliver on this policy objectives are naturally supported by NEXIM Bank.

The allusion to giving loans to some beneficiary big U.S. companies to establish cronyism accusation is not well-founded. Between 2007 and 2014, loans to SMEs accounted for 68% of the total portfolio of the U.S. Ex-Im. While a few organisations have dominated the list of beneficiary big firms, it is not without justification.

Companies like Boeing and Caterpillar are manufacturers of expensive heavy duty equipment and machines. The equipment and machines are very much needed in the delivery of public works and infrastructure projects in Africa and in other developing regions that are witnessing an economic renaissance.

Accordingly, these firms are bound to generate big-ticket transactions which will require some of the financing tools at the disposal of the Ex-Im Bank to consummate. The same argument more or less holds for the involvement of General Electric which, in recent times, has shown interest in the investment opportunities of sub Saharan Africa’s infrastructure and electric power. The proactive investment of GE in the SSA power sector ensures it is a reliable vehicle and partner for the delivery of President Obama’s Power Africa Initiative.

To be fair, the U.S. Ex-Im Bank has discharged its mandate creditably. The institution has inspired establishment of similar export credit agencies around the world. The Bank seems to have entered a new phase whereby it would play a more active role in boosting trade between the U.S. and Africa in general, and U.S. and Nigeria in particular. NEXIM Bank is in a collaborative relationship with U.S. Ex-Im and several other ECAs with the aim of sharing knowledge and capacities. This will require strengthening the U.S. institution after its charter has been renewed for long-term.

By Roberts Orya: Managing Director / CEO, Nigerian Export-Import Bank (NEXIM)

It is clear to see that Mr. Godwin Emefiele has demonstrated preparedness for his current position as Governor of Central Bank of Nigeria than what analysts may have acknowledged. During his confirmation-hearing before the Senate, Mr. Emefiele said his regime at the CBN will make banking count for development.

Since assumption of office, he has made concrete policy commitments to back his assertion that finance should have strong connections to development. One can safely expect that more actions in this regard will follow in the course of his time in office.

Mr. Emefiele’s position has long been validated by the International Labour Organisation (ILO) as well as the United Nations at various times and through various pronouncements and declarations.

Since 2007, long before the financial and economic crisis, the ILO has maintained its position regarding the role of central banks in controlling inflation and promoting job creation. The point is, despite precarious levels of unemployment and under-employment in the developing world, many central banks in those regions have not seriously considered employment creation as part of their mandate. Instead, they have narrowly interpreted monetary policy to mean just stemming the tide of inflation through inflation-targeting and price stabilisation.

Godwin Emefiele CBN Governor

As has been established by development experts, it is now trite for central banks to limit monetary policy solely to price stabilisation. This is notwithstanding the fact that this alone cannot guarantee that economic growth will improve since low inflation does not necessarily lead to higher income and a stable economy. Nor does a high rate of economic growth necessarily lead to a high rate of employment creation.

This is especially the case in Nigeria where we have witnessed impressive GDP growth rates over the past seven years without a corresponding reduction in the unemployment rate, which rose to 23.9 per cent in 2012 relative to 13.9 per cent in 2000.

Indeed, in his presentation at his maiden press briefing, “Entrenching Macroeconomic Stability and Engendering Economic Development in Nigeria,” Mr. Emefiele disagreed with the dominant school of thought that sees the role of central banking as being limited to achieving low inflation as a policy strategy for growth, increase in employment, and poverty reduction. He audaciously stated that the CBN under his leadership would also begin to include the unemployment rate as one of the key variables considered for its Monetary Policy decisions.

To truly create a ‘people-oriented Central Bank’ as envisaged by the Governor, the issue of access to finance by Micro, Small and Medium-scale Enterprises (MSME) needs to be quickly addressed. The weak connection between banking and development in Nigeria is expressed in the remarkably low access to financing by the MSMEs; difficulties in accessing financing by women entrepreneurs; paucity of long-term funding for real sector operators; high cost of credit across the business spectrum, owing to prohibitive interest rates; general low banking penetration; and weak grassroots banking due to very limited success of microfinance banks. Without a doubt, these issues are impediments to economic growth and development. MSMEs are generally regarded as drivers of innovation. They are also reckoned as the engine of economic growth across developing and advanced economies.

In China’s vibrant economy, SMEs account for 99.9% of total number of firms, and they provide 84% of total employment (World Bank, 2013). Inadequate funding for this sector in Nigeria has long been diagnosed as an impediment to innovation, employment generation and economic growth.

Another frontier of growth is women entrepreneurship. Empirical data has shown that women are increasingly getting involved in business formation. This global trend has gained even more momentum in developing countries where women, from time, have been known to be very enterprising in the agrarian economy and in trade.

But notwithstanding, around the world, women still very much lag behind men in business ownership. Businesses operated by men tend to be more successful. Apart from the myriad of social forces that militate against the success of women entrepreneurs relative to men, lack of access to financing has been somewhat intractable. Primordial prejudices against women have shifted only in some little ways. Thus, disparity in access to financing based on gender is unfavourable to women.

The funding structure in the economy also calls for interventions in real sector activities. Manufacturers of different stripes turn to Nigerian Export – Import Bank (NEXIM Bank) with the same requirement. They want long-term financing at affordable, or preferably, single-digit interest rates.

But the funds to supply credit under these conditions are hardly available in the market. The lending environment is defined by tight monetary stance, which has seen the Monetary Policy Rate remaining at 12% in the past two years, in order to stymie inflationary pressure.

In tandem, yields on risk-free government securities are in lower double digits. Moreover, low-cost deposit mobilisation by commercial banks remains aspirational due to low level of household savings and low banking penetration. (Only about 25% of the population is banked.)

As for the microfinance segment, it would be apposite to have the following hypothesis tested. One of the consequences of the rapid pace of urbanisation over the years is that renewal of the economically-active population in rural and suburban settings has been impeded.

As such, microfinance is being addressed to the urban poor while the rural poor are chronically underserved. But social identification which influenced traditional practice of micro lending and drove positive repayment behaviours is absent in the cities. For that reason, microfinance banks have especially struggled to make significant impact and remain in business.

This general context to financing in Nigeria has meant that commercial banks are hardly taken to be agents of development. This perception needs to change through the implementation of policies that underpin the role of banking in the development process.

It is, therefore, appropriate and also commendable that Mr. Emefiele has construed the role of the CBN as making banking particularly relevant to development. Central banks have policy tools to make this happen. The CBN governor has hinted on his intent to deploy a variety of such tools.

The MSME Fund

In August, President Goodluck Jonathan launched the Micro, Small and Medium-scale Enterprises fund. Promoted by Central Bank of Nigeria, the N220 billion fund has become the first concrete step under the regime of Mr. Godwin Emefiele to deliver on his promise that the CBN will be an agent of development. The MSME fund spared none of the issues that have been enumerated above. While the size of the Fund means that it will not meet all the needs; it can provide the basis for scaling up the interventions in one form or another.

The MSME sector comprises an estimated half a million operators. Operators in the sector collectively account for about 50% of Nigeria’s GDP, according to the Minister of Commerce, Trade and Investment, Mr. Olusegun Aganga.

However, only 8% of the MSMEs in Nigeria are reckoned to have access to financing. This underscores the importance of this Fund which will lend at single-digit interest rate. With significant funding, it is imaginable that, like the data from China, MSMEs in Nigeria can contribute over 90% of the GDP.

The MSME Fund is not necessarily a novel idea in Nigeria. There have been similar initiatives in the past, which achieved little success. But here is a situation where past failures should not be a hindrance to new efforts. The stakes are higher now for the success of the MSME sector. Because of the large number of the firms, they not only constitute the engine of growth for the economy, they will also create millions of jobs and therefore alleviate poverty.

To put this in context, it has been acknowledged that micro, small and medium scale enterprises tend to employ the poor including those without formal qualifications; and the enterprises are usually the only hope of employment in rural communities. Even so, most poor and unskilled people only get by through self-employment.

It is no surprise the CBN governor has worked really hard to launch the MSME fund with presidential backing and as quickly as he did. He has restated time and again his determination to link Nigeria’s economic growth to job creation.

Around the world and in the country, policymakers are weary of “jobless growth” because of high unemployment rates. Instead, they are pressing for inclusive, job-oriented economic growth models. Global employment rates have raised concerns, but not merely because employment has again played the role of the laggard in recovering from the last economic downturn.

Unemployment is also associated with social risks, and a move towards full employment is critical for inclusiveness and shared prosperity.

By design, 60% of the MSME Fund is allocated to women entrepreneurs. This is good news for gender advocates and those who care about inclusivity. The fund is a necessary boost for women entrepreneurship.

I agree completely that women are the new frontier for finance. The women folk have long been deprived of access to credit. Whereas women are adept at business formation, mostly in order to improve the living conditions of their family, they are less successful in business. Their greater dedication to family life poses a limit to their business success.

But beyond this, lack of collateral, often based on gender discrimination, especially in land and property ownership, has meant that women have lesser access to financing for their businesses.

However, women are proven to be better money managers. Their success is also known to have more impact on the family than when men are the bread winners. This, therefore, means that women can make more contributions to development if they are empowered with financial access.

Working through the DFIs

The decision of the CBN governor to work with development finance institutions is of particular interest to NEXIM Bank, and Nigerian exporters in the non-oil sectors.

Although the development finance segment of the Nigerian finance industry is in the early stage of transformation, the DFIs have garnered some experience to help deliver development outcomes in their areas of focus.

NEXIM has been working with SMEs in our sectors of focus — Manufacturing, Agro-processing, Solid minerals and Service – under what we call the MASS Agenda. Our interest has been to help nurture indigenous businesses in the MSME sector to become global players, by financing their production and export capabilities.

From our experience, the “MASS” sectors are in the frontline of employment generation, and they are mostly characterised by low barriers for new entrants. This means that interventions in these sectors can quickly scale up.

It is very heartening to note that President Goodluck Jonathan has been an ardent supporter of the DFI community in Nigeria. This undoubtedly will translate to fiscal support for the agenda of the CBN Governor for intervention in the quest for development in the country.

We saw this in the housing sector with the launch of Nigerian Mortgage Refinance Company earlier in January. As already noted, the MSME programme received presidential attention, with Mr. President being physically present at the launch of the fund.

Also, the Co-ordinating Minister for the Economy and Finance Minister, Dr. Ngozi Okonjo-Iweala has already hinted last June, at the dinner organised by the African Development Bank (AFDB) to flag-off events marking its 50th anniversary that the Federal Government was fine-tuning plans to establish a Nigerian Development Bank in 2015.

This is in addition to other programmes by the Administration that will restructure and strengthen development finance institutions in Nigeria to enable them scale up results and close the gaps in development financing.

NEXIM Bank is very enthusiastic on these brighter prospects.

By Chinedu Moghalu: Head of Corporate Communication

Nigerian Export-Import Bank (NEXIM)

Nigeria is not just a place to set up a business. The country is a big and growing market. Investing in Nigeria is tantamount to connecting to a big market.

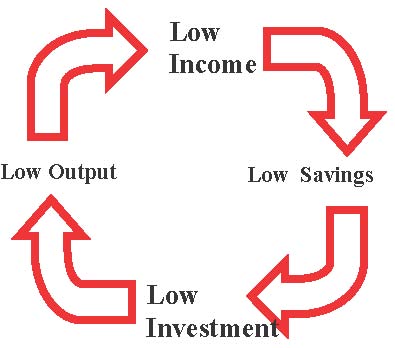

The Vicious Circle of Poverty

The relationship between trade and poverty is inverted. Countries with higher proportions of global trade tend to have less of poverty. Conversely, countries which contribute the least to global trade have higher poverty rates.

This shows the importance of good trade policies in reducing poverty rates and increasing prosperity. Also, this shows why there is intense competition for export markets even by countries that already control significant share of global trade. Little wonder trade facilitation has become an economic policy of great importance. Development experts can’t agree more.

The vicious circle of poverty

Jim Yong Kim, the World Bank president, said in a recent statement that, “Trade is a critical component to ending poverty and boosting shared prosperity.” The foregoing therefore suggests that developing countries have to trade their way out of poverty. For African countries to reduce poverty, they must increase their share of global trade. But how to bring this about is anything but easy.

Trade Challenge

Sub-Saharan Africa is reputed to be the least developed region of the world. The SSA region is also the least integrated into the global economy through trade.

Since the 1960s, the share of sub-Saharan Africa in international trade has become progressively smaller: less than 5% for all merchandise and 3% for agricultural products in 2010 (World Foundation for Agriculture and Rurality 2012).

Trade within the SSA region is also dismal. Tariff and non-tariff barriers have been obstacles to intra-regional trade. Although the higher hurdles are non-tariff barriers, the ECOWAS goal of free movement of person and goods across member countries remains more of a wish than reality.

Exports from Africa are mainly mineral resources and agricultural produce. With very low industrial base, the commodities are exported to other regions of the world and returned later to the continent as costlier finished products.

This trade pattern results in “jobless growth” in the exporting countries when the prices of the commodities are high in the international market. The jobs that are created and sustained during commodity boom are mainly in the countries that “refine” and turn the commodities to finished products through industrial activities.

But when prices of commodities are depressed, fiscal shocks are transmitted through the trade channel to the exporting countries, with severe human and economic implications. Apart from being pro-cyclical, trade in commodities is generally noted for volatility of current account positions and exertion of pressure on the exchange rate.

The persistence of weak or negative growth in Europe and slower growth in China has dented economic growth in countries that depend very much on the export markets including Germany. But this does not build a case against active play in the export markets; it probably asserts the importance of domestic consumption as a cushion during a period of weaker exports.

Export Diversification

Having established the role of trade in reducing poverty on the one hand, and the deleterious effects of export of mainly primary products on the other, it therefore means that the way to reduce poverty in developing countries is through export diversification by boosting industrial activities.

Gaining a mileage in export diversification does entail formalisation of informal trade. To achieve this, empowerment of small- and medium-scale enterprises (SMEs) is of utmost importance, both in itself and in gaining more share of global trade.

The key problem with informal trade is that it deprives policy-makers of the major tool of policy-making, which is data. Informal trade usually takes place off the radar, making data gathering and processing virtually impossible.

But policy-makers need to know areas where it is important to scale up positive results in trade activities. Understanding the obstacles that confront informal sector operators will aid intervention and will eventually prepare the operators toward making due contribution to fiscal policy by coming under the tax net.

SME Incubation

Evidently, the Administration of President Goodluck Jonathan has identified the SME sector as critical for boosting economic growth and job creation.

On its part, the Nigerian Export – Import Bank (NEXIM Bank) is aware of the potential of Nigerian SMEs. They can leverage domestic consumption, using access to over 170 million population to harness opportunities in foreign markets.

Accordingly, our interventions are now geared towards such firms that we believe are relatively well-structured to be able to stabilise their operations and then foray into external markets.

Several programmes under this Administration are incubating the SME segment for a major turnaround. In the traditional areas of providing infrastructure and electricity power, the country is seen to have made big leaps in policy formulation and execution, notwithstanding the milestones that are yet to be reached. Most recent perhaps is the launch of the N220 billion SME fund by the President in August, under the auspices of Central Bank of Nigeria. Specific programmes under the Agricultural Transformation Agenda, infrastructural development for ICT utilisation, local content development in oil and gas, the programme of industrialisation as encapsulated in the National Enterprise Development Programme (NEDEP) and the Nigerian Industrial Revolution Programme (NIRP) all speak of the resolve of President Jonathan to use the instrumentality of state policy to mediate market performance and SME growth. On-going implementation of the programmes is concomitant with job creation, which is vital for eradication of extreme poverty.

Unmasking Poverty

Poverty eradication has once again climbed to the top of global development policy agenda. The World Bank and the International Monetary Fund (IMF) have announced twin programmes of ending extreme poverty and boosting shared prosperity by 2030.

Feelers from post-2015 policy debates suggest that global development goals will focus on eradication of extreme poverty, going forward from next year. In the meantime, reports from some global institutions are making some important prescriptions on poverty reduction.

A recent publication by United Nations Conference on Trade and Development (UNCTAD) – Trade Policies, Household Welfare and Poverty Alleviation: Case Studies from the Virtual Institute Academic Network – strongly associates trade and poverty, offering policy-makers insights on what it called “pro-poor trade policies.”

Another new literature which focuses on economic growth – a sine qua non for poverty reduction – reaffirms what we already know: that export diversification is the “gateway” to higher growth. To achieve export diversification however, Chris Papageorgiou, Lisa Kolovich and Sean Nolan, all of the IMF, identify manufacturing of high quality products as a necessity.

They suggest therefore that the world has gone past the Chinese industrialisation model of producing cheap and low quality products to unleash price competition in the export market. Accordingly, Chris and his colleagues listed human capital, infrastructure, institutional quality, financial deepening and proximity to markets as drivers of export diversification. These are very important recommendations which are familiar but which cannot be overemphasized. I will therefore run commentaries on them in the context of the Nigerian policy environment and readiness for trade as I conclude this piece.

Quality Products: The Nigerian middle class and wealthy Nigerians are noted to be pretty sophisticated. As such, an industrial development model that manufactures cheap and inferior products would be mis-targeted at Nigerians with means.

Nowhere is this recognised more than in the cable manufacturing industry where Nigerian cables are noted for higher quality than some imported brands. Once known for exporting inferior products, China has been reforming its industrial policy to emphasise the manufacturing of high quality products. This is the direction Nigeria should go to ensure we can trade in the global market of today and not of yesterday.

Human Capital: Within a practical framework, multi-level support for human capital development has been a key goal of this Administration. School enrolment has improved generally. Specific programmes have targeted areas that had lagged behind due to past neglect. Tertiary education is being strengthened to be able to absorb more university candidates.

Another area that has benefited from government’s programme of industrial development is vocational education. For example, there are on-going efforts to develop skills that will support growth in the power sector and automobile production and assembly plants.

Also, the Subsidy Reinvestment and Empowerment Programme (SURE-P) embeds training for skill acquisitions in the areas of public works, including road construction and maintenance, railway rehabilitation and dredging.

Infrastructure: The foregoing already highlights the fact that the country is moving in the right direction with infrastructure development. The pace may be slow, but there is no doubt that we will attain a tipping point sooner than later. At that point, it will become more obvious to global investors that so-called infrastructure deficiency in Nigeria represents investment opportunities which are being harnessed. This is a key lesson we have taken from the implementation of the power sector reform.

Institutional Quality: The truth is evident that Nigeria is building and strengthening its institutions again. As a constitutional democracy, the governance framework is stable and predictable. Market regulators do their jobs without the fear of any political backlash. This is what has helped to put in place a sustainable path for the turn-around of our financial market, since the introduction of reforms in 2004. NEXIM Bank itself is an institution that has been revamped as part of government decision to strengthen public sector institutions and support private sector actors.

Financial Deepening: There is perhaps no other country or jurisdiction that has introduced more far-reaching reforms in its financial market than Nigeria over the past ten years. The proliferation of marginal banks has given way to stronger and sounder private sector financial institutions including “mega” banks. A poorly organised and unfunded pension system has given way for the contributory system that has exceeded N4.5 trillion ($24 billion) in pension asset. Yet regulation and innovation have continued to characterise the Nigerian financial system, including the capital market.

Proximity to Markets: Nigeria is not just a place to set up a business. The country is a big and growing market. Investing in Nigeria is tantamount to connecting to a big market. Nevertheless, the country is also well-linked to the sub-regional markets by all popular means – road, sea and air – except by rail.

As the country continues to develop capacity for trade through economic diversification, it is expected that the poverty rate will continue to fall.

By Roberts Orya: Managing Director / Chief Executive Officer, Nigerian Export – Import Bank (NEXIM).

• ICT engineer turned career diplomat endorsed as ‘safe pair of hands’ to steer ITU through its next four years.

ITU’s 19th Plenipotentiary Conference roundly endorsed Houlin Zhao of China as its next Secretary-General. Zhao will take office on 1 January, 2015 for a term of four years, with the possibility of re-election for one additional four-year term.

The election took place in Busan, Republic of Korea, during the Plenary session of the PP-14 conference.

Zhao won the position with 152 votes, from 156 ballot papers deposited. He contested the position unopposed.

Houlin Zhao

Addressing the conference after the vote, Zhao told some 2,000 conference participants from around the world that he would do his best to “fulfil ITU’s mission, and, through our close cooperation, ensure ITU delivers services to the global telecommunication and information society at the highest level of excellence.”

Zhao is a respected telecoms engineer with over 30 years’ experience in the international environment. He currently serves as ITU Deputy-Secretary-General (DSG), a post he has held since January 2007 after being elected by ITU’s 2006 Plenipotentiary Conference in Antalya, Turkey. He was re-elected for a second four-year term at ITU’s 2010 Plenipotentiary Conference in Guadalajara, Mexico.

In his two terms as DSG, Zhao has charted a steady course for the organization, pioneering new initiatives to expand ITU membership to the global academic community, and proactively implementing efficiency improvements in human resources management and financial administration.

He is well-known and well-regarded by the global ICT community, both for his technical expertise and his commitment to digital inclusion for all.

Prior to his role as Deputy, Zhao served two elected terms as Director of ITU’s Telecommunication Standardisation Bureau (TSB), the part of ITU most concerned with developing global technical standards to ensure worldwide interoperability of information and communication equipment and software.

Before that, he was for 12 years a Senior Counsellor with TSB, and its former incarnation, CCITT.

Houlin Zhao: Biodata

Born in 1950 in Jiangsu, China, Mr. Zhao graduated from Nanjing University of Posts and Telecommunications, and holds an MSc in Telematics from the University of Essex in the UK.

From 2007 to 2014, he served as ITU Deputy Secretary-General, supporting the work of the Secretary-General, principally in terms of day-to-day management, including human resources, financial administration, improving efficiency, and working to help broaden ITU’s membership, particularly in terms of academic institutions.

From 1999 to 2006, he served as Director of ITU’s Telecommunication Standardisation Bureau (TSB). During his term of office he spearheaded the introduction of new efficiency measures to improve ITU’s standards-making environment and strengthen its promotion. He also enhanced the strategic partnership between Member States and Sector Members, while initiating and maintaining good relationships with industry members. Under his leadership, ITU enhanced its level of international co-operation with other standards development organisations, and was instrumental in helping bridge the standardisation gap between developing and developed countries.

From 1986 to 1992, Zhao was a senior staff member in the then CCITT, and from 1993-1998 in TSB. Among his responsibilities as Counsellor for ITU-T Study Groups, he was Co-ordinator for co-operation with other international technical bodies, including ISO and IEC.

Prior to joining ITU, Zhao served as an engineer in the Designing Institute of the Ministry of Posts and Telecommunications of China, taking an active role in his country’s expert meetings on telecommunication standards and national plans, as well as participating in ITU’s technical Study Group meetings as a Chinese delegate. He contributed important articles to a number of prestigious Chinese technical publications, and in 1985 was awarded a prize for his achievements in science and technology within the Ministry of Posts and Telecommunications.

I am deeply honoured to be the Guest Speaker at this public lecture because I see it as a forum that will enhance public awareness of the existence of risk as a natural phenomenon to human existence.It should also draw our attention to the fact that we all — individuals and governments — have a responsibility to manage risk, for the betterment of our lives and those of the people we serve.

We are often impervious to the risks we face on a daily basis. Risk here being the probability or the threat of damage, loss, injury or any other negative occurrence that is caused by external or internal vulnerabilities, the consequences of which may be avoided through preemptive action.

Gov. Fashola

In other words, it can simply be described as the probability of losing something of value for example physical health, property or social status. Risk management refers to the steps we take to mitigate or eradicate the risk.

As a government, we are responsible for the well-being and welfare of the people we serve. We have a responsibility to provide social security for both the young and the elderly; a responsibility to provide security of life and property and also a responsibility to ensure that the Infrastructure put in place are properly maintained in a way and manner that the State can be described as having a ‘developed economy status’.

Where we fail to take pre-emptive steps to attend to the risks that come with the responsibilities that have been placed on us, we would be failing in a part of our duty as Government.

The Lagos State Government has always been in the vanguard of identifying risks and taking steps to mitigate/eradicate those risks, as much as possible. To list a few, the Climate change risks which could expose the State to flooding and other natural hazards but which we have successfully mitigated in the past few years; Health Risks such as that recently posed by the incursion of Ebola Virus Disease to Nigeria, against which prompt steps were taken by the State Government to curtail the spread of the disease.

We also face security challenges: kidnapping, ritual killings, armed robberies etc. These are threats to peaceful co-existence of inhabitants of the State. To mitigate those risks, the Lagos State Government equipped the Rapid Response Squad and other Law enforcement agencies.

Our youth and the elderly are exposed to social protection risks which if not addressed could result in poverty, and other security hazards in the community.

Furthermore, risks of danger to lives and property of the citizens exist where, due to unprofessional practices on the part of those involved in construction, substandard materials are used in construction.

On this front, the Lagos State Government realized that the risk faced is in two folds: i.e. risk to life and property and secondly the risk of the construction being delayed or never completed due to a variety of reasons which would have an ultimate negative effect on the environment.

The Lagos State Government’s risk mitigation response to this was the establishment of agencies to regulate/supervise building projects in the State. In order to ensure that delays in construction projects do not create severe adverse occurrences, it embraced Insurance as a risk transfer mechanism.

The business of Insurance, simply put, is to ensure that full or partial financial compensation is made for loss or damage caused by events beyond the control of the insured.

It is a contractual agreement between two parties i.e. the insurer and the insured, under which the insurer covenants to indemnify the other party against a specified amount of loss, occurring within a specified period, provided that the premium is paid. It is designed to put the insured back in the position, or at least as close as possible, in which he or she was before the occurrence of the loss.

In essence, it is expected that gains are not made from Insurance arrangements and to be able to insure a risk, the insured must have insurable interest over the tangible or intangible asset.

In Lagos State, largely based on the Nigerian Insurance Act 2003, certain insurance policies are specified as compulsory insurances that must be arranged and these are:

• The Group Life Assurance Scheme in line with the 2004 Pension Reform Act.

• Builders Liability Insurance

• Occupiers Liability Insurance

• Motor Third Party Insurance

• Health Care Professional Liability Insurance under the National Health Insurance Act of 1999

On the issue of pensions, you will agree with me that before the Pension Reform by the Federal Government in 2004, our pensioners faced the risk of a life of penury due to the unfunded nature of the Pay as you Go Pension Scheme in the public service and the lack of provision of pension arrangements for employees in the private sector.

The risk of the elderly not having financial independence and dying in poverty was real and to eradicate this risk, on the 19th of March, 2007, the Lagos State Government subscribed to the fully funded Contributory Pension Scheme.

It imposed on us a huge liability as we needed to pay of 7.5% of basic salary, housing and transport allowances as monthly pension contribution; fund the Retirement Bond Redemption Fund Account with 5% of employees monthly total emolument figure to provide for accrued pension rights, being entitlements for years spent in service before the commencement of the contributory pension scheme. monthly; pay the annual premium to guarantee the life assurance cover as stipulated in the Law and which is intended to provide a death benefit of at least 3 times the annual total emolument of each employee.

We are, however, committed to making Lagos State Government a government that cares for the welfare of the people, and is prepared to stand with them through difficulties that are occasioned when certain risks crystallise.

We remain resolute in our desire to identify areas that may hinder the peace of mind of the populace and hence we have invested Billions of Naira towards ensuring that the retirees receive monthly income as pension from their pension provider who could be the Pension Fund Administrators or the Life Assurance Companies who provide annuity for the lifetime of the retirees.

The Lagos State government has also sought to support the growth of a viable insurance industry by ensuring that it keeps its own insurance policies current and settles its premiums as and when due.

But beyond our role as government, in order to ensure that more people embrace insurance, even beyond the compulsory, the Insurance Industry needs to do a lot more to create awareness of the benefits of transferring risks through Insurance.

A lot of trust also needs to be built and this will only be achieved where the principle of utmost good faith and duty of disclosure, which are key Insurance Principles, are practiced by the Insurance Companies.

Conclusion

In conclusion, I wish to commend the National Association of Insurance Correspondents on this 1st Public Lecture on Insurance & Pensions.

This I believe is a step in the right direction and should be sustained. The Industry needs the awareness; the people need to develop the confidence; the Industry needs to rise more stoutly to her responsibility as risk bearers; we need a re-orientation and a re-definition of core values for which our society will be the better.

Thank you for listening.

Eko o ni baje o.

Babatunde Raji Fashola, SAN, Governor of Lagos State

ADDRESS DELIVERED BY HIS EXCELLENCY, MR. BABATUNDE RAJI FASHOLA, SAN, GOVERNOR OF LAGOS STATE, AT THE 1ST PUBLIC LECTURE ON ‘THE ROLE OF GOVERNMENT IN MANAGEMENT OF RISKS IN THE SOCIETY’ ORGANIZED BY THE NATIONAL ASSOCIATION OF INSURANCE CORRESPONDENTS AT THE ABORA-MAZONIA SUITE, EKO HOTELS & SUITES, VICTORIA ISLAND, LAGOS ON TUESDAY, 28TH OCTOBER, 2014.

The Ebola Virus Disease (EVD) pandemic has gripped the world like no other scourge in decades. For medical experts, what makes Ebola more dangerous than others before it is the high fatality rate and ease of spread, which results in rapid death of infected persons and multiple transmission between individuals.

And for the global insurance industry, Ebola represents yet another scourge on the balance sheet of insurance companies as claims could arise rapidly to provide succour to families of victims.

In this report, we present various angles of the effect of EVD on the insurance industry.

• Insurance Industry Ramifications of the Spread of the Ebola Virus- Dr. Steven N. Weisbart, CLU

Current Situation

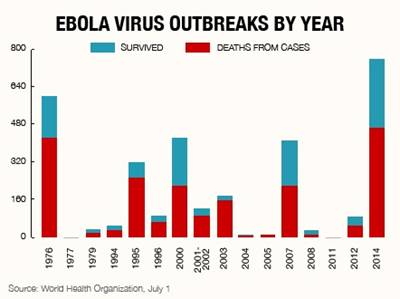

• As of October 10, the Ebola virus has infected at least 8,399 people and killed 4,035, according to the World Health Organisation. This includes 4,762 confirmed cases, 2,196 probable cases and 1,652 suspected cases.

• As of October 10, all but four of the cases were in four countries in Africa (Guinea, Liberia, Sierra Leone, and Nigeria). One was in Senegal, one in Spain, and (as of October 12) two in the United States.

• There are five known strains of the Ebola virus. The one causing the illness and deaths noted above is the Zaire strain, which was identified in 1976.

• There is currently no cure and no vaccine for this virus. Treatment is isolation (to prevent spread) and focus on symptoms—mainly dialysis and fluids to prevent dehydration and reduce fever.

• The mortality rate of infected people to date is roughly 50 percent.

• Unlike influenza viruses, the Ebola virus is transmitted only by contact with an infected person’s bodily fluids (e.g., blood, saliva, sweat, diarrhea, vomit, etc.) during the incubation period or shortly thereafter. Contact with the fluids could be from contact with sheets, mattresses, medical equipment or any other surface to which the fluids were transferred.

Expected Near-term Health-care Situation

• In the U.S., the Centers for Disease Control and Prevention (CDC) does not expect the Ebola virus to infect people other than a small number of health-care workers and others who have had direct contact with the bodily fluids of an infected person.

• However, the CDC is investigating the confirmed case (on October 12) of a health-care worker in Dallas who had treated an infected person, because it does not know how the health-care worker acquired the virus, and this might suggest weaknesses in the isolation/prevention protocols.

Worst Case Scenario

If the number of cases in Africa continues on its exponential ascent, the number of people who might carry the virus elsewhere around the world will also grow. The number of cases in Africa is likely to grow if isolation of the sick, tracking their contacts, and careful procedures followed by health-care workers, proves to be inadequate. An especially concerning scenario is the travel of infected people from Africa to India,

China or other heavily populated countries, where there are billions of people living in many densely-populated cities with relatively weak health-care systems.

Another element of a worst-case scenario would be screening systems at U.S. and other ports of entry that are ineffective in identifying people carrying the virus. This was how both the U.S. and Spanish cases gained entry into their respective countries. If improvements in screening are not completely effective, additional infected individuals could enter countries around the world, potentially leading to the spread of Ebola in the developed world and beyond.

Another threat is the possibility that the virus could mutate into one that is more virulent—producing a higher death rate. This might also increase the ease of spread of the virus.

Effect on Life and Health Insurance

• The effects on the Life and Health insurance industries will clearly depend on whether the infected people are insured. Some of those who have died up to now were children and almost certainly did not have life insurance.

• Even if the Ebola virus spreads to infect tens or even hundreds of thousands of adults in Africa, it is not likely to trigger many life insurance or health insurance claims there. Life insurance coverage in the three most affected countries—Guinea, Liberia and Sierra Leone—is extremely low. Indeed, in Swiss Re’s most recent report on life premiums per capita (for 2013), the calculation for all three of these countries are so small that none makes the list.

• Even in the unlikely event that the Ebola virus spreads to infect tens of thousands of adults in the United States, the financial impact will likely be quite manageable. This is because perhaps one-third of adults in the U.S. have life insurance only through their employment, and the amount is typically equal to one year’s income. Another one-third have individual life insurance, with the average death benefit in the $200,000 range. In a typical year life insurers pay about 2 million death claims, so another 100,000 would be only 5 percent more than typical. Moreover, most life insurers are well capitalized, and even the largest life insurers have reinsurance to prevent a surge in death claims from imperiling their solvency, so that the net effect would likely be, at most, a reduction in the profit they would otherwise record.

• The cost of caring for Ebola cases would likely be at the high end of health insurance claims, and the effect on health insurers would depend on the number of people suspected of being infected. Many people would need to be tested to see whether they have contracted the virus, and the cost of isolation of those affected could be substantial. Note that some individuals may have no health insurance, as was the case with the index (first) patient who died of Ebola at a Dallas hospital on October 8. In such cases, treatment costs will likely be borne outside the private health insurance system.

Effect on Property/Casualty Insurance

• The main effect on the Property/Casualty insurance industry would likely be on companies writing Workers Compensation insurance because health-care workers could be most directly exposed (as happened in Texas and in several African countries). Workers Compensation pays for the cost of medical care and lost income for people who become ill in the course of their work, and pays death benefits if they die from a work-related cause. As with life insurance, it is unlikely that many workers in the main affected African countries have workers compensation-type coverages; the latest Swiss Re report indicates that the level of premiums per capita for all non-life insurance coverages combined (not just Workers Compensation) in the three most-affected countries is so low as to not be listed. In the United States, in contrast, Workers Compensation coverage is nearly universal, but the likelihood of claims is low, assuming that employers and their workers take CDC-recommended precautions. As with life insurance coverage, reinsurance will help mitigate the financial effect of a surge in claims, which are likely to be very costly in the event of actual work-related infections.

• Other possible effects might be on various liability insurance lines. These include General Liability, Directors & Officers (D&O) Liability and Medical Malpractice (Med Mal) Liability. General liability and D&O claims might be filed asserting that the policy owner was negligent in failing to prevent transmission of the virus. For example, a claim might be filed alleging negligent disposal of contaminated waste, pursuing either General Liability or Med Mal recovery. Med Mal claims might assert that proper medical protocols were not followed, resulting in infection by the Ebola virus, or that the disease was not properly diagnosed or diagnosed in a timely manner or that the treatment protocol itself and/or care rendered was somehow negligent. At this stage it is impossible to forecast the precise number of such claims or the amounts of damages that might be sought. That said, assuming the CDC’s protocols are successfully followed, the number of Ebola cases should be small, thereby limiting the number and likelihood of tort actions that can impact various liability coverages.

Life insurance marketing and sales materials go through many internal hoops before consumers ever see them. That starts at point of creation and continues on through legal and compliance review, production and distribution. What’s more, all must be done within budget and on time. But what happens once consumers see the materials?

Scott Kallenbach, Research Director, LIMRA Strategic Research, posed that question during a workshop recently at LIMRA’s Annual Meeting in New York.

Sometimes, people just draw a blank. That may have something to do with all those internal hoops.

To reach consumers, company materials “need to focus on outcomes,” Kallenbach said during an interview in advance of his talk. That is, they need to focus on how consumers perceive the content and meaning, instead of focusing on the output.

Focus on Consumer Understanding

What’s important is the customer understanding that comes from reading and seeing the materials, he indicated.

Agents need to focus on this too, he said. For instance, “it’s important that they explain a piece they are presenting to a customer in layman’s terms.”

To increase this understanding, companies and agents need to shift their focus in four key communications areas, Kallenbach said. They need to:

–Put attention on the information that consumers retain, not on the amount of information delivered.

–Provide disclosure in a context that people can understand rather than concentrate on providing complete disclosure.

–Make the content “intentional,” in the sense that it tells consumers what they need to know in language they can understand, not just on making the content defensible in a legal sense.

–Take a one-to-many “sharing” perspective which highlights how insurance enables people to share risk with many others, as opposed to a one-to-one perspective, which presents purchase and ownership as disconnected, singular activities.

Opportunity to Connect

When consumers can’t understand or retain the messages from their insurers, the industry loses the opportunity to connect, Kallenbach indicated.

To illustrate, he pointed to what happens when men go to buy an engagement ring. Most men walk into the jewelry store already knowing that the value of the ring should be equal to two or three times their monthly salary, the LIMRA executive said. Men know this because of a successful consumer-focused marketing campaign by the famous diamond cartel, De Beers.

That company put the purchase of a diamond engagement ring into “a context — the pay check — that people can understand,” Kallenbach said.

LIMRA is currently talking with insurance executives about doing something similar, he noted. The discussions are exploring what message will instill a sense of confidence and comfort with insurance.

The industry does have rules of thumb for, say, withdrawal percentages from retirement accounts and for recommended multiples of salary for life insurance, he allowed. But the discussions now underway are looking beyond multiples for an overriding message.

Make it Understandable

A point he kept revisiting during the interview is that the language the industry uses in many of its consumer materials is not understandable for a lot of people.

Life insurance content can be very formal and often includes jargon, he said. It would be more effective if it were conversational, with the focus on “telling the customers what they need to know.”

Too many times, industry communications do not align with that consumer perspective, for instance about protecting the family. In fact, he said, “our language can be intimidating.”

About his one-to-many suggestion, Kallenbach pointed out that the concept of sharing is popular today. Consumers like the idea that everyone “puts in a little bit” so that someone with a need can be helped.

That’s what people today call “collaborative consumption,” he said. It was the insurance industry that came up with the concept a long time ago, he added, but “we don’t get credit for it.”

Kallenbach suggested the industry highlight the concept now. For example, it could focus more on how adopting a healthier lifestyle helps not only the individual, who gains better health, but also the insurance pool that shares the risk.

Sometimes stories help, he noted. He recounted how two brothers whom he knows were planning to apply for life insurance. They decided to compete to see which one would get a better insurance rate. Their means of competition was adoption of healthier lifestyles — diet, exercise and the like. In the end, one did get a better rate than the other, Kallenbach said. But both brothers are continuing their healthier regimen to this day. It’s been two years now, and counting.

About legal and Compliance

Will use of more conversational language and context-guided disclosure put insurance communications in the crosshairs of insurance company legal and compliance teams?

“It would be great if marketing, compliance and legal could work together early in the process, to help consumers understanding together,” he said.

It’s important for everyone to follow the rules and the laws, he added. “But we need to put this into context for the consumer.”

A recent study of 1,500 consumers that LIMRA did jointly with Maddock Douglas found that the words, images and messages the industry uses to explain financial products don’t seem realistic or relatable to many consumers. What’s needed, the researchers found, is “authentic communication” that is easy to understand, down to earth, memorable, positive, credible and relevant.

According to Maria Ferrante-Schepis, Managing Principal-Insurance and Financial Services Innovation at Maddock Douglas and a Co-presenter with Kallenbach at the workshop, internalising authentic language provides a major innovation opportunity.

VIEWS FROM ABROAD

Question: What is the top life insurance trend or issue that will dominate the business in 2015?

“The top issue is the agency field force and our inability to attract new talent. Everyone is talking about how this is happening due to changing demographics. Well, the demographics are not changing. They have already changed. The changes include increased diversity, cultural shifts, the growth in women who have more spending power, and the way Gen- X and Gen-Y communicate and buy, and what their expectations are.

The life insurance industry needs to address the change or sales will continue to decline. Specifically, we need to change the way we sell to adequately address these changes.”

— Barbara Turner, CEO of Onesco and Chief Compliance Officer for Ohio National Financial Service, Cincinnati, Ohio.

The top issue will be finding efficient ways to reach the middle market with the goal of selling more insurance to this market. The reason is, the middle-market is severely underinsured and uninsured. I served in product development, agent training and marketing roles for insurance companies for 26 years, so I know that we tried as an industry to reach this market by advertising, but that didn’t work.

We need to change the experience so that we draw the middle-market buyers in. We have to change the process to something they will like so that they will ultimately buy. Too often, buying life insurance is a long process. You have to learn about it, make a choice, fill out pages of questions, ask your doctor to send the reports, and wait for things to happen; sometimes you have to wait two or three months. Many carriers are experimenting with this right now. For the last six months, I’ve been with a data analytics company; we’re bringing solutions that could help the carriers with this.

In a general sense, we need to find the right way to reach the middle market at the right time with the right message.”

“In view of all the changes we are seeing in technology, distribution, and decreased sales of life insurance, the top issue will be how to engage the consumer. We have difficulties in connecting so that consumers can access products and services in new ways.

This is a problem in my country, Canada, as well as in the United States. Consumers today connect on the web, and the legacy systems don’t impact them. The industry needs to connect in different ways that draw them closer.

A lot of this LIMRA conference is about thus issue. We need to access the middle-market in a cost effective way, whether that involves phone, internet, or changing approaches that make it so that insurance is not sold but rather bought. We need make changes so that people want to buy.”

• UN Secretary-General, WBG, IsDBG Presidents, other Agency Heads Visit Region to Link Peace Efforts with Economic Progress

Leaders of global and regional institutions today begin an historic trip to the Horn of Africa to pledge political support and major new financial assistance for countries in the region, totaling more than $8 billion over the coming years. UN Secretary-General Ban Ki-moon, the World Bank Group (WBG) President, Jim Yong Kim, as well as the President of the Islamic Development Bank Group and high level representatives of the African Union Commission, the European Union, the African Development Bank, and Intergovernmental Agency for Development (IGAD) are combining forces to promote stability and development in the Horn of Africa.

On the first day of the joint trip, the World Bank Group announced a major new financial pledge of $1.8 billion for cross-border activities in a Horn of Africa Initiative that will boost economic growth and opportunity, reduce poverty, and spur business activity.

The initiative covers the eight countries in the Horn of Africa — Djibouti, Eritrea, Ethiopia, Kenya, Somalia, South Sudan, Sudan, and Uganda.

“This new financing represents a major new opportunity for the people of the Horn of Africa to make sure they get access to clean water, nutritious food, health care, education, and jobs,” said World Bank Group President Jim Yong Kim. “There is greater opportunity now for the Horn of Africa to break free from its cycles of drought, food insecurity, water insecurity, and conflict by building up regional security, generating a peace dividend, especially among young women and men, and spurring more cross-border cooperation.”

Leading the trip to the Horn of Africa, the United Nations Secretary-General, Ban Ki-moon said “The countries of the Horn of Africa are making important yet unheralded progress in economic growth and political stability. Now is a crucial moment to support those efforts, end the cycles of conflict and poverty, and move from fragility to sustainability. The United Nations is joining with other global and regional leaders to ensure a coherent and coordinated approach towards peace, security and development in the Horn of Africa.”

The European Union also announced that it would support the countries in the region with a total of around $3.7 billion until 2020, of which about 10 percent would be for cross-border activities; the African Development Bank announced a pledge of $1.8 billion over the next three years for countries of the Horn of Africa region; while the Islamic Development Bank committed to deploy up to $1 billion in new financing in its four member countries in the Horn of Africa (Djibouti, Somalia, Sudan and Uganda).

The Horn is diverse, with some of the fastest growing economies and huge untapped natural resources. However, it also has many extraordinarily poor people and populations that are now doubling every 23 years. Unemployment is widespread among growing numbers of young people. Women, in particular, face huge obstacles because of their gender, including limited land rights, limited education, and social customs that often thwart their ability to pursue economic opportunity, and improve living conditions for their families and communities.

Countries in the region are also vulnerable to corruption, piracy, arms and drug trafficking. Terrorism, and related money flows are significant and interconnected threats in the Horn of Africa. People-trafficking is also a growing problem in the region. However, there are commendable efforts being made through regional cooperation in parts of the Horn to tackle the root causes of these problems.

The new financing announcement will support those efforts and comes on the first day of the trip led by UN Secretary-General Ban Ki-moon, to discuss peace, security, and resilience. In addition to the UN Secretary-General, other leaders making the trip are World Bank Group President Jim Yong Kim; Islamic Development Bank Group President Ahmad Mohamed Ali; African Union Commission Deputy Chairperson Erastus Mwencha; Intergovernmental Agency for Development (IGAD) Executive Secretary, Ambassador Mahboub Maalim; African Development Bank Group Special Advisor to the President, Youssouf Ouedraogo; Deputy Director General for Development and Cooperation, European Commission, Marcus Cornaro and European Union Special Representative for the Horn of Africa, Alexander Rondos.

The World Bank Group said its new $1.8 billion packaging, which is in addition to its existing development programs for the eight countries, would create more economic opportunity throughout the region for some of the most vulnerable peoples, including refugees and internally displaced populations and their host communities. Wars and instability have generated more than 2.7 million refugees along with over 6 million internally displaced people. The Bank Group will also help the region build up its communicable disease surveillance, diagnosis, and treatment capacity.

Many of these diseases are associated with or exacerbated by poverty, displacement, malnutrition, illiteracy, and poor sanitation and housing. Increased cross-border trade and economic activity in the Horn of Africa will necessitate simultaneous investments in strengthening disease control efforts and outbreak preparedness.

The Bank Group will also support greater regional links between countries with regional transport routes, stronger ICT and broadband connectivity, more competitive private sector markets, increased cross-border trade, regional development of oil and gas through pipeline development, and the expansion of university and other tertiary education.

The Bank Group’s pledge includes $600 million from the IFC, its private sector arm, which will support economic development in the countries of the Horn. IFC investments under the new Horn Initiative will include a regional pipeline linking Uganda and Kenya; greater investment in agribusiness expansion in storage, processing, and seeds; possible public-private partnerships in pharmaceuticals, renewable energy and transport; and financial advice and support to government and companies to improve business confidence and investment, access to markets, and access to private finance. Another $200 million is for guarantees against political risks from the Multilateral Investment Guarantee Agency.

A new World Bank Group paper forecasts that the Horn will undergo dramatic and lasting change when oil production starts in Kenya, Uganda, and possibly Somalia and Ethiopia.

For its part, the European Union’s Horn of Africa approach is based on a strategic framework adopted in 2011. Support programs for 2014-2020 will be guided by the same analysis that underpins the World Bank’s Horn of Africa Initiative and will focus on the development challenges that must be tackled to unlock the region’s considerable potential. EU support will mostly target the three pillars of the Horn of Africa Initiative: boosting growth, reducing poverty by promoting resilience, and creating economic opportunities.

“The EU stands ready to further deepen its long-standing partnership with the Horn of Africa – helping to build robust and accountable political structures, enhancing trade and economic cooperation, financing peace keeping activities and providing humanitarian assistance and development cooperation,” said European Development Commissioner Andris Piebalgs prior to the trip.

Other leaders on the trip said that the Horn of Africa region needs new development assistance in order to secure peace and opportunity to thrive and prevent future conflicts.

The Islamic Development Bank Group said its new financing for Djibouti, Somalia, Sudan and Uganda over 2015-2017 would focus on critical infrastructure development, food security, human development, and trade. A further $2 billion could be provided by the Arab Coordination Group over the same period.

Commenting on this announcement, Islamic Development Bank Group President Ahmad Mohamed Ali said “The Horn of Africa is an important gateway to Africa and a bridge to Western Asia. Bringing stability and sustainable development to the Horn of Africa will undoubtedly significantly contribute to stability across the entire African continent. The Islamic Development Bank Group salutes this renewed focus on the Horn of Africa and stands ready to work with all partners, including the Arab Coordination Group, to support regional cooperation and the economic revival of the Horn of Africa, especially in its four member countries.”